At a busy roadside stall in Nairobi, a small food vendor realizes she is running out of stock just as the lunch rush begins. Instead of closing early or borrowing from friends, she pulls out her phone and, within minutes, money hits her account. There are no forms to fill out, no guarantors to find, and no collateral required.

Behind that instant loan approval is not a bank officer, but an automated system powered by artificial intelligence. In just seconds, the system reviews her transaction history, how often she sends and receives money, how regularly she pays bills, and how well she manages her daily cash flow. Using this information, it quickly determines whether she qualifies for a loan.

This has become common across Kenya as millions of people can now access credit not because of what they own, but because of how they handle their finances. In the past, traditional lending excluded many people who lacked pay slips, bank statements, or physical assets. Today, artificial intelligence is changing this by turning everyday mobile transactions into a reliable financial record that is used to evaluate whether one is qualified or unqualified for a loan.

What Is AI Credit Scoring?

Credit scoring is a risk-evaluation tool lenders use to determine whether a borrower is likely to repay a loan or default. Traditionally, this process relied on a limited set of financial indicators, such as credit history, income, and existing debts, to evaluate a person’s reliability.

Technology has refined this process using artificial intelligence. A study by Kitrum (2025) provides that “AI credit scoring is a process of evaluating the creditworthiness of an individual using machine learning, which is used to analyze much larger and more complex sets of data, including both financial and behavioral information. Instead of depending on a few fixed factors, these systems can review large amounts of data in real time, identify patterns that may not be obvious, produce faster, more accurate results, and help in making a lending decision.”

A new survey by the Central Bank of Kenya highlights the rapid adoption of artificial intelligence in credit risk assessment. While only about half of Kenyan lenders have adopted AI so far, 65% of those that have already used it have used it specifically to evaluate borrower risk. Digital credit providers are leading this shift, with around 80% relying on AI-based scoring systems, followed by microfinance banks at 75%, while commercial banks are further behind at 45%.

How AI Uses M-Pesa Data to Approve Loans

On platforms such as M-Pesa, millions of transactions generate a continuous stream of financial data. Artificial intelligence systems analyze this data to make real-time credit decisions. To explain how AI achieves this, this part is divided into three sections: the types of M-Pesa data AI analyzes, the behavioral patterns it examines, and the process by which it makes lending decisions. Each of these parts is explained below.

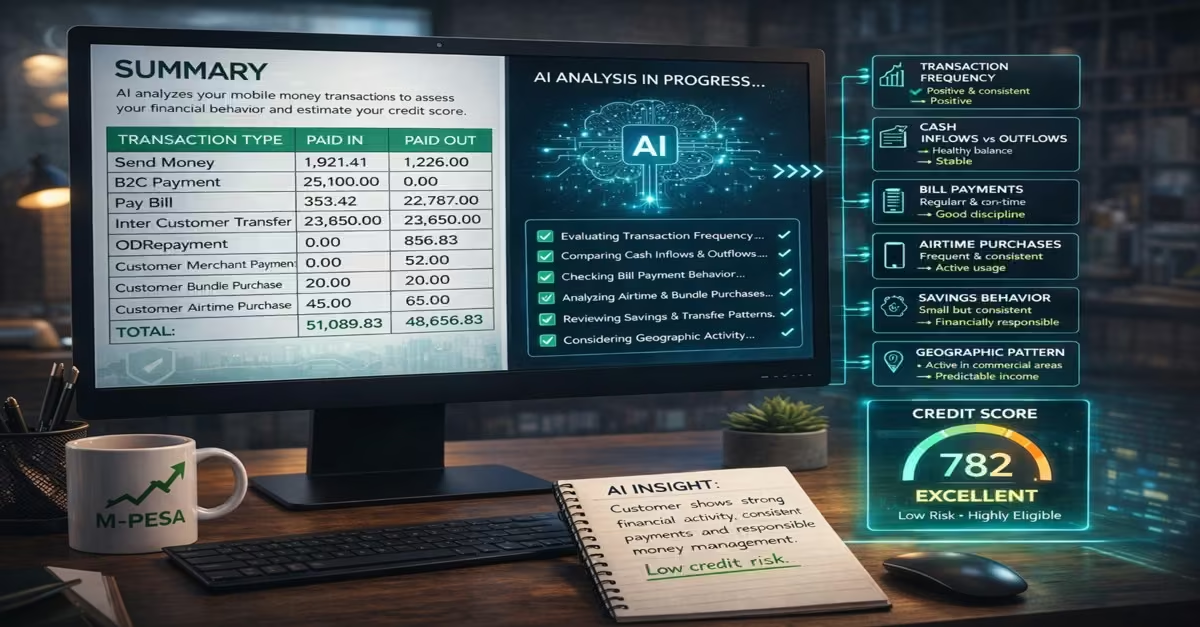

Types of Data Analyzed in AI Credit Scoring

AI credit scoring relies on a wide range of data points drawn from everyday financial activity, especially through platforms like M-Pesa. Understanding these data types reveals how lenders build a more accurate and inclusive picture of a borrower’s creditworthiness.

a) Transaction Frequency

This refers to how often a user sends, receives, or moves money through platforms like M-Pesa. High and consistent transaction activity signals that the user is financially active, which increases confidence in their ability to repay a loan. In contrast, irregular or minimal activity may indicate a higher risk.

b) Cash Inflows and Outflows

AI systems analyze the amount of money coming in (cash inflows) versus what is being spent or sent out (cash outflows). A healthy balance where inflows regularly exceed or sustain outflows suggests financial stability. This helps lenders estimate whether a borrower has enough liquidity to meet repayment obligations when they fall due.

c) Bill Payments

Regular payment of bills such as electricity, water, rent, or subscriptions is a strong indicator of financial discipline. AI models assess not just whether bills are paid, but also how consistently and on time they are, using this as a proxy for repayment behavior.

d) Airtime Purchases

Frequent and consistent airtime top-ups may seem minor, but they provide valuable behavioral insights. They indicate active mobile usage and can reflect income patterns, spending habits, and financial regularity, especially for users without formal banking records. A frequent and consistent airtime top will signal greater financial ability to repay the loan, making you less risky.

e) Savings Behavior

AI evaluates whether a user sets aside money over time, either through mobile wallets like M-swari or KCB, or through linked savings products. Consistent saving even in small amounts demonstrates financial planning and discipline, which lowers perceived credit risk.

f) Geographic Patterns

Location data is used to understand your economic environment and activity, such as the level of commercial activity in a region, which helps AI better estimate earning potential and financial consistency. Consistent activity in certain areas, such as business districts, will make AI a predictable income source and contribute to economic stability, reducing the chances of default and, in turn, credit risk.

Read Also: The Rise of AI-Powered Marketing Tools

Behavioral Patterns AI Looks For

Beyond raw transaction data, AI credit scoring focuses heavily on behavioral signals to also assign you a credit score. This data helps assess current financial status and predict future repayment behavior. A study by Mihir (2025) highlights the following behavioral data that AI uses.

a) Consistency of Income

AI evaluates how regularly a user receives money, whether daily, weekly, or monthly. Consistent inflows, even if relatively small, signal a stable income stream and reduce lenders’ uncertainty. On the other hand, irregular or unpredictable earnings may indicate higher risk, as repayment capacity becomes less reliable.

b) Financial Discipline

Financial discipline reflects how well a user manages their available funds. AI analyzes spending habits, budgeting patterns, and overall cash flow behavior. Indicators such as maintaining a positive balance, avoiding unnecessary withdrawals, and paying bills on time suggest responsible financial management. Strong financial discipline increases a borrower’s digital creditworthiness and improves their chances of loan approval.

c) Repayment Behavior

One of the most critical factors in AI credit scoring is how a borrower has handled past credit obligations. AI examines whether loans were repaid on time, partially settled, or defaulted. A history of timely repayments and responsible borrowing builds trust with lenders and strengthens a borrower’s profile. In contrast, late payments or defaults significantly reduce creditworthiness, as they directly signal repayment risk.

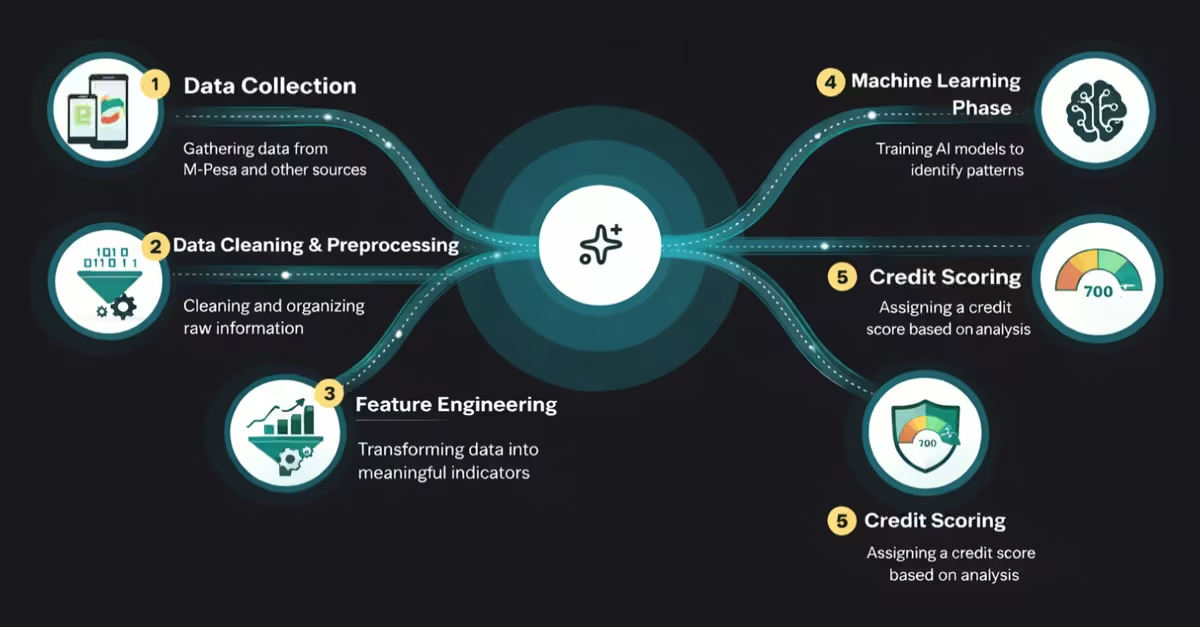

How AI Credit Scoring Works

AI credit scoring follows a structured, step-by-step process that transforms raw mobile money data into lending decisions used by various financial institutions. Below is how artificial intelligence used the data collected to assign you a specific credit score.

a. Data Collection

The process begins by gathering data from sources like M-Pesa. This includes transaction history, bill payments, airtime purchases, merchant payments, and cash flow records. As discussed above, both financial and behavioral data are collected to build a comprehensive user profile.

b. Data Cleaning and Preprocessing

Raw data is often messy and incomplete, so AI systems first clean and organize it. Errors, duplicates, and inconsistencies are removed, and the data is standardized into a usable format. This step ensures accuracy before any analysis begins.

c. Feature Engineering

Feature engineering is the process of selecting and preparing data so that an AI model can learn more effectively and make more accurate predictions. It usually involves turning raw data into useful information for AI. At this stage, raw data is transformed into meaningful indicators. For instance, transaction history is converted into metrics like income consistency, spending patterns, savings trends, and financial discipline.

d. Machine Learning Phase

AI models are trained using historical data from past borrowers who repaid and those who defaulted. Using this, the model can identify patterns that predict creditworthiness. For example, consistent income and timely bill payments are weighted positively, while irregular cash flow or excessive withdrawals may signal high credit risk.

e. Credit Scoring

The AI model assigns a credit score or risk rating based on the analyzed data. This score directly informs the lending decision whether to approve or reject the loan. It determines key terms such as loan amount, interest rate, and repayment period.

Benefits of AI Credit Scoring

AI credit scoring represents a major improvement in how lending systems work. By using data and machine learning, it solves many of the challenges found in traditional credit models, providing faster, smarter, and more inclusive financial services. The following are the major benefits it brings, as per Laura (2025)

- Speed – One of the clearest advantages is speed. AI-powered systems can quickly analyze large amounts of data and make lending decisions within seconds, enabling near-instant loan approvals on platforms like M-Pesa. This eliminates the long wait times common to traditional loan applications.

- Accuracy – AI improves credit assessment accuracy by simultaneously reviewing multiple data points and behavioral patterns. This helps lenders better predict risk, reducing the likelihood of lending to high-risk borrowers and lowering default rates.

- Inclusivity – Unlike traditional credit scoring, which depends heavily on formal financial records, AI makes it possible for people without a banking history to access credit. Using alternative data, such as mobile money transactions, creates financial opportunities for millions who would otherwise be left out of the system.

- Cost Efficiency – AI reduces the need for manual work, paperwork, and large operational teams. This lowers the overall cost of lending for financial institutions, making it easier for them to offer more affordable, scalable loan services.

- Real-Time Decision Making – AI systems work in real time, meaning they assess creditworthiness using the most recent data available. This allows lenders to make timely decisions and adjust loan terms as a borrower’s financial behavior changes.

- Scalable – AI-driven systems can process millions of loan applications simultaneously without slowing down. This makes it easier for lenders to grow their services and reach more customers, especially in fast-growing markets like Kenya.

Risks and Challenges of AI Credit Scoring

While AI credit scoring is transforming access to finance in Kenya, it also introduces new risks that cannot be ignored. Understanding these challenges is essential to ensure that innovation does not come at the expense of consumer protection. A study by Laura (2025) highlights the following challenges.

a) Data Privacy Concerns

AI credit scoring relies heavily on personal and transactional data from mobile money platforms like M-Pesa. This raises important concerns about how user data is collected, stored, and shared. Without strong data protection frameworks and enforcement, there is a risk of:

- Unauthorized access to sensitive financial information

- Misuse of personal data by third parties

- Lack of user consent or awareness.

As digital lending grows, data privacy will remain a critical issue for both regulators and consumers.

b) Lack of Transparency (The “Black Box” Problem)

Many AI models operate as “black boxes,” meaning their decision-making processes are not easily understood, even by the institutions using them. As a result:

- Borrowers may be denied loans without clear explanations

- It becomes difficult to challenge or appeal AI decisions.

- Users may not know how to improve their credit profile.

This lack of transparency can reduce trust in digital lending systems and highlights the need for explainable AI in finance.

c) Algorithmic Bias and Fairness

AI systems are trained on historical data, which may contain hidden biases. If not carefully managed, these biases can be reinforced by the algorithm, leading to unfair outcomes. For example:

- Certain groups may be unintentionally disadvantaged.

- Lending decisions may reflect past inequalities.

Even without deliberate intent, this can result in discriminatory lending patterns, raising concerns about fairness and inclusivity.

d) Over-Reliance on Algorithms

As AI becomes more accurate and efficient, there is a growing risk that financial institutions may rely too heavily on automated decision-making. This can reduce human oversight, especially in complex cases where:

- Context matters more than raw data

- Exceptional circumstances need consideration

- A balanced approach that combines AI efficiency with human judgment is often more reliable.

e) High Default Risks in Digital Lending

Although AI is designed to reduce credit risk, the speed and ease of accessing digital loans can sometimes lead to higher default rates. This is mainly caused by the:

- Borrowers may take loans impulsively

- Credit may be extended too quickly

This creates a situation in which access grows faster than repayment capacity, posing risks for both lenders and borrowers.

f) Over-Borrowing and Digital Debt Cycles

Instant access to credit can encourage repeated borrowing, especially among users with limited financial literacy. Some borrowers may:

- Take multiple loans from different apps

- Use new loans to repay existing ones

This can create digital debt cycles in which individuals become trapped in continuous borrowing, resulting in financial stress.

Read Also: How Modern Technology Is Reducing Financial Fraud in the Digital Age

How to Improve Your Digital Creditworthiness

As AI credit scoring becomes more common, your everyday financial behavior, especially through platforms like M-Pesa, directly affects whether you qualify for a loan. Improving your digital credit profile does not require complicated steps; it mainly involves building consistent and responsible financial habits over time.

a) Maintain Consistent Transaction Activity

Regularly sending, receiving, and managing money demonstrates financial activity. Consistent transaction activity helps AI systems build a clear and reliable profile, making you appear more trustworthy to lenders.

b) Show Stable Income Patterns

Try to ensure that money comes into your account steadily and predictably—whether daily, weekly, or monthly. Even small but regular inflows can show financial stability and improve your chances of getting approved for a loan.

c) Pay Bills on Time

Paying bills such as electricity, water, or subscriptions on time shows strong financial discipline. AI systems consider this a key sign that you are likely to repay loans responsibly.

d) Repay Loans on Time

Your loan repayment history is one of the most important factors. Paying on time—or even earlier than required—helps build a positive credit profile. It increases your chances of qualifying for larger loans in the future.

e) Avoid Multiple Simultaneous Loans

Taking multiple loans at once can signal financial pressure and increase your risk. It is better to manage and clear one loan before taking another to maintain a strong and healthy credit profile.

Conclusion

AI credit scoring is significantly changing how lending works in Kenya, shifting the focus from traditional collateral to trust built through data and everyday financial behavior. Through platforms like M-Pesa, millions of transactions are now used as strong indicators of creditworthiness. These transactions include your transaction frequency, cash inflows and outflows, airtime purchases, bill payments, savings behavior, and geographical patterns. While this innovation has created new opportunities for people without formal banking histories and made lending more efficient for financial institutions, it also raises important concerns, including data privacy, transparency, responsible borrowing, algorithmic bias, high default rates, and the risk of over-borrowing. To improve your AI credit score, you need to maintain consistent transactions on M-Pesa, show stable income, pay bills on time, repay your loans on time, and avoid multiple loans.