In recent years, the financial industry has changed how it operates. Businesses are continually looking for new ways to improve customer experiences and make financial transactions simpler and more efficient than before. Nowadays, you can easily apply for insurance, acquire credit, and make payments without ever leaving the app or platform you are already using. This smooth integration of financial services into non-financial platforms is known as embedded finance.

Understanding Embedded Finance

Embedded finance is the integration of financial services such as lending, payments, insurance, and banking into non-financial platforms like e-commerce websites, mobile applications, ride-hailing services, and digital marketplaces to enable users to access financial services exactly when and where they need them without switching to a separate banking application as per Alex (2025). This innovation allows customers to access financial tools at the exact moment they need them within a digital experience. For example, an online marketplace may allow customers to complete payments within the app without leaving the platform.

What makes embedded finance different from traditional banking services is the way financial capabilities are delivered to users. Customers usually had to interact directly with banks or separate financial applications to make payments, apply for loans, or manage other financial services within traditional banking systems. Embedded finance removes this extra step by integrating these services directly into the platforms where transactions already occur, thereby improving user convenience and enabling businesses to deliver smoother, more efficient digital experiences to their customers.

How Embedded Finance Works

Embedded finance operates through a collaborative ecosystem in which several specialized participants work together to deliver financial services within non-financial platforms. The system used here depends on partnerships between financial institutions, fintech innovators, infrastructure providers, and customer-facing companies. Each participant performs a specific role that enables financial services to be delivered smoothly within everyday digital experiences. A study by Priority Commerce highlights the roles of each part in the operation of embedded finance.

a) Fintech Platforms

Fintech platforms are financial technology companies that design and develop digital financial products such as mobile banking applications, digital wallets, lending services, and peer-to-peer payment applications. Within the embedded finance ecosystem, fintech companies act as innovators, creating user-friendly financial solutions and integrating them across various digital platforms. However, most fintech firms do not operate as fully licensed banks. Instead, they collaborate with regulated financial institutions to provide services legally and securely.

b) Sponsor Banks

They are also known as partner banks; they are licensed financial institutions that provide the regulatory foundation required for embedded finance services. These banks hold the necessary banking licenses and ensure that financial activities comply with regulations such as anti-money laundering rules and consumer protection laws. Sponsor banks may include Equity Bank, Kenya Commercial Bank (KCB), and Cooperative Bank. These banks then collaborate with fintech companies to extend banking capabilities into digital platforms. Because they are responsible for regulatory compliance, sponsor banks carefully evaluate their partnerships and closely monitor financial programs. Through these partnerships, fintech companies can offer services such as payment processing, account management, and lending while operating under the bank’s regulatory framework.

c) Technology Providers

Technology providers play an important role by supplying the infrastructure that connects fintech platforms with sponsor banks. Many of these companies operate through Banking-as-a-Service (BaaS) models and provide application programming interfaces (APIs) that enable seamless integration between financial systems and external platforms, as per Alex (2026). APIs enable developers to embed banking features such as payment processing, identity verification, and account management directly into digital applications. In addition to connectivity, some technology providers also offer services such as transaction monitoring, fraud detection, and risk management tools.

d) End-Brands

End-brands are the businesses and digital platforms that customers interact with directly. These companies integrate financial services into their existing products or platforms, allowing users to access financial features without leaving the application. For instance, some e-commerce platforms have integrated payment systems directly into their marketplaces. A good example is Jumia, which has embedded JumiaPay directly into the Jumia application to allow customers to shop online, pay bills, and top up airtime seamlessly within the same platform. Together, these participants form a coordinated ecosystem that allows financial services to be embedded into everyday digital interactions. Through the collaboration of fintech innovators, regulated banks, technology infrastructure providers, and customer-facing platforms, embedded finance enables businesses to deliver convenient financial solutions while maintaining regulatory compliance and operational efficiency.

Read Also: How Modern Technology Is Reducing Financial Fraud in the Digital Age

Types of Embedded Financial Services

Embedded finance includes a variety of financial services that can be integrated directly into digital platforms. Instead of requiring users to leave an app or website to access financial tools, businesses have seamlessly integrated these services into their existing platforms. This approach allows companies to improve the customer experience, simplify transactions, and create new revenue opportunities.

a) Embedded Payments

Embedded payments are one of the most common forms of embedded finance. They allow customers to complete transactions directly within a platform without being redirected to external payment systems. They are mainly used in online marketplaces, where users pay for products instantly through built-in payment systems, and in ride-hailing platforms, which enable passengers to pay for trips automatically through the app. By integrating payment processing into their platforms, companies reduce interruptions during checkout and speed up transactions for users.

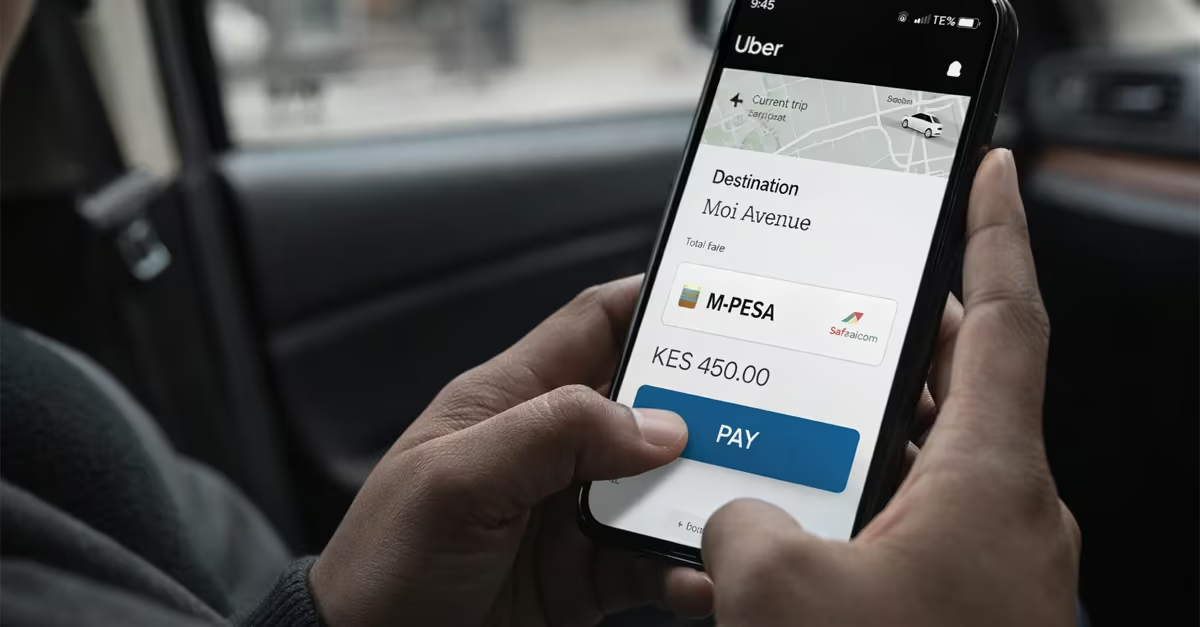

A practical example is provided by staff writers, who note that in Kenya, there is integration between Uber and M-Pesa. Uber is primarily a ride-hailing and delivery platform rather than a financial institution, yet through its partnership with Safaricom, riders can pay for trips directly within the Uber app using M-Pesa. Drivers can also receive their earnings through the same mobile money platform. This integration removes the need for riders to leave the Uber app to complete payments through M-Pesa separately, while also giving drivers, especially those without traditional bank accounts, direct access to digital payouts. By embedding M-Pesa into its platform, Uber demonstrates how non-financial digital services can seamlessly integrate financial capabilities, thereby improving convenience.

b) Embedded Banking Accounts

Embedded banking services enable companies to offer banking-like features, such as digital accounts, debit cards, and money management tools, within their platforms. In Kenya, embedded banking is available on digital platforms such as Chipper Cash, the Send App by Flutterwave, Wave, and Airtel Money. These platforms provide users with digital accounts or mobile wallets within their applications, allowing them to store funds, transfer money, and make payments without relying entirely on traditional bank accounts. For example, Chipper Cash provides users with a free digital account that supports international transfers and digital payments, while Airtel Money allows customers to deposit funds, pay bills, send money, and sometimes access microloans directly within the mobile money ecosystem.

c) Embedded Insurance

Another rapidly growing area of embedded finance is embedded insurance, in which customers can purchase coverage directly at the point of sale. Instead of searching for insurance separately, coverage is offered on the same platform where a product or service is purchased. For example, when booking a flight, reserving a hotel, or buying a new car, customers may be presented with travel insurance, protection plans, or warranty coverage during checkout. This approach allows users to obtain the protection they need immediately and more conveniently.

A Daily Whistle report indicates that when customers book flights online, they are often offered travel insurance at checkout. This insurance covers risks such as trip cancellations, medical expenses, and lost luggage while they are travelling, without requiring them to visit a separate insurance provider. This seamless integration allows customers to obtain insurance instantly within the same platform they already use, demonstrating how non-insurance businesses can embed financial protection services to make access easier, faster, and more convenient for users.

d) Embedded Lending

Embedded lending allows platforms to provide credit or financing options directly to customers or businesses at the point of transaction. Embedded lending occurs when credit products are integrated directly into digital platforms such as mobile money services, apps, or e-commerce systems. Instead of applying for loans separately through banks, users can access financing within the platforms they already use for payments or transactions. In Kenya, common examples include M-Shwari, which allows users to borrow directly within M-Pesa, and Fuliza, an overdraft facility embedded in M-Pesa transactions. Another common example of embedded financing is buy now, pay later (BNPL) services offered at checkout on e-commerce websites, which allow customers to split payments into installments instead of paying the full amount at once. In Kenya, Buy-Now-Pay-Later services allow consumers to purchase products immediately and repay the cost over time through digital platforms. Examples include Faraja by Safaricom, SpotIt by Craft Silicon, M-KOPA’s pay-as-you-go financing, and Aspira’s installment-based purchasing model. These services integrate credit directly into mobile payments and retail transactions, making them examples of embedded finance as highlighted by Elvy (2025)

e) Embedded Investment Services

Some platforms integrate investment services that let users save or invest money without leaving the app. For instance, fintech apps allow users to invest small amounts of spare change from purchases into investment portfolios or offer simple stock investment options within a digital wallet. These embedded investment features help make investing more accessible to everyday users by integrating it into platforms they already use frequently.

Business Benefits of Embedded Finance

As digital commerce and online platforms continue to expand, many businesses are adopting embedded finance to improve their services and stay competitive. By integrating financial tools directly into their platforms, businesses provide a smoother and more convenient experience for customers while also opening new growth opportunities. As Velina’s (2024) research illustrates, the following benefits.

- Improved Customer Experience-One of the most important advantages of embedded finance is its ability to enhance the overall customer experience. When financial services such as payments, financing, or insurance are built directly into a platform, users can complete transactions without leaving the app or website they are using. This reduces interruptions during the purchasing process, making transactions faster and more convenient.

- New Revenue Streams-Embedded finance also creates new income opportunities for businesses. Businesses can generate additional revenue through transaction fees, partnerships with fintech providers, or commissions from financial services such as lending and insurance.

- Increased Customer Loyalty-When financial services are seamlessly integrated into a platform, customers are more likely to continue using it. This is because embedded finance creates a more convenient and engaging ecosystem where users can complete several activities in one place. For example, a ride-hailing platform that allows users to pay for rides, store funds in a digital wallet, and receive rewards within the same app can encourage repeat use. This convenience helps strengthen customer relationships and increases long-term loyalty.

- Faster Transactions-Embedded finance can significantly speed up transactions by eliminating reliance on external payment systems or manual financial processes. Payments can be completed instantly within the platform, reducing delays and improving operational efficiency for businesses.

Benefits for Consumers and End Users

Embedded finance not only benefits businesses but also greatly improves the financial experience for consumers. By integrating financial services directly into digital platforms, users can make payments, access credit, and manage financial activities within the same environment where they shop, book services, or interact online. This integration removes many of the traditional obstacles associated with banking and financial transactions, making financial services faster, more accessible, and easier to use. The following are the benefits it brings to the consumers.

- Convenience and Seamless Payments

One of the biggest benefits of embedded finance for consumers is the ability to make payments smoothly, as it allows users to pay directly within apps or websites without switching to external banking platforms.

- Faster Access to Credit

Embedded finance also provides faster and easier access to credit. Many platforms now offer financing options, such as buy now, pay later services. Instead of applying for loans through traditional banks, consumers can access credit directly at the point of purchase. This allows users to spread payments over time or obtain short-term financing quickly, making it easier to manage larger purchases.

- Integrated Financial Management

Another benefit is the ability to manage financial activities within a single platform. Embedded financial tools such as digital wallets, payment histories, and account balances allow users to track their transactions without switching between multiple financial applications. For example, drivers working through Uber in Kenya can receive payments, track their daily and weekly earnings, and review trip histories directly within the same platform where they provide ride-hailing services. The app records completed trips, automatically calculates fares, and shows drivers their total income, allowing them to manage their work and finances in one place.

- Personalized Financial Services

Because embedded finance platforms often analyze user data and transaction patterns, they can offer more personalized financial services. Platforms may provide tailored financing options, targeted promotions, or customized financial recommendations based on a user’s behavior and preferences. This level of personalization helps consumers access financial products that better suit their needs.

- Reduced Friction in Digital Transactions

Embedded finance significantly reduces the barriers commonly associated with traditional financial processes. Instead of filling out long forms, visiting bank branches, or navigating multiple applications, users can complete financial transactions quickly within the platform they are already using. This simplified approach makes everyday financial activities such as paying for products, purchasing insurance, or accessing credit much easier and more efficient for consumers.

Read Also: TikTok Marketing in Kenya: How Businesses Can Grow Online

Challenges and Risks of Embedded Finance

While embedded finance offers many opportunities for innovation and business growth, it also introduces several challenges and risks that need to be managed by businesses, as the integration of financial services into the various digital platforms will require businesses to comply with regulations, as now the business will be handling sensitive customer data and ensuring they are working on secure technological systems. A study by Rayanna (2025) highlights the following challenges.

a) Data Privacy Concerns

One of the main challenges of embedded finance is protecting user data. Because these systems process sensitive financial and personal information, platforms must ensure that customer data is collected, stored, and handled securely. Any misuse or unauthorized access to financial data can harm customer trust. It may also result in legal penalties, so businesses that implement embedded finance must adopt strong data protection practices and comply with privacy regulations to safeguard user information.

b) Cybersecurity Threats

Embedded finance platforms are also vulnerable to cybersecurity risks, including hacking, fraud, and data breaches. Since financial transactions occur directly on digital platforms, cybercriminals may exploit system weaknesses to access payment data or disrupt services. To reduce these risks, businesses must invest in strong cybersecurity measures such as data encryption, multi-factor authentication, and continuous system monitoring to protect both their platforms and their users.

c) Regulatory Compliance

Financial services are heavily regulated in many countries, and embedded finance solutions must comply with applicable financial laws and regulations. Businesses that offer financial services through their platforms may need to comply with consumer protection, anti-money laundering (AML), and know-your-customer (KYC) rules. Understanding and following these regulations can be challenging, especially for non-financial companies entering the financial services sector.

d) Complexity in Integrating Multiple Services

Integrating financial services into digital platforms is a complex process that requires strong technological infrastructure and careful coordination between multiple participants. Businesses must ensure their systems can support advanced financial features without disruption, often by leveraging application programming interfaces (APIs) and partnerships with banking institutions. Seamless backend integration is essential to prevent technical issues and ensure that financial services operate smoothly within the platform, avoiding delays, errors, or service interruptions that can damage customer trust.

e) Dependence on Third-Party Fintech Providers

Many embedded finance solutions rely on partnerships with fintech companies, Banking-as-a-Service providers, or external payment processors. While these partnerships make it easier to integrate financial services, they also create dependence on third-party systems. If a fintech provider experiences technical difficulties, regulatory challenges, or operational failures, it can directly affect the platform offering the embedded financial service. For this reason, businesses must carefully choose reliable partners and establish strong service agreements to minimize potential risks.

Conclusion

Embedded finance has changed how financial services are delivered in the digital economy. By integrating payments, lending, insurance, and banking capabilities directly into non-financial platforms, embedded finance enables businesses to deliver seamless financial experiences within the apps and services people already use. Despite the benefits of embedded finance, business and end users must also understand the risks it entails. These risks include data privacy concerns, as much customer data is collected, cyber security threats, compliance difficulties, and the complexity of integrating multiple services.