Debt is one of the most powerful tools in modern finance. When used carefully and with clear planning, it helps a business grow faster, expand into new markets, and invest in opportunities that would not be possible using only internal funds. Through financial leverage, the businesses borrow funds to increase potential returns, such as profits, grow their operations, and improve returns to shareholders. In highly competitive markets, taking on debt is often an important strategy for maintaining competitiveness and driving growth.

Financial leverage is the strategic use of debt in a business’s operations to generate profits that exceed the cost of borrowing. In this way, leverage can help a business increase profits when a company earns more from its investments than it pays in interest, and it can also increase losses when performance weakens. Many entities misunderstand leverage by paying too much attention to short-term growth figures and return on equity, while giving less attention to important risks such as liquidity problems, the pressure of regular debt repayments, exposure to rising interest rates, and unstable cash flows. This uneven focus can create the false impression that a company is financially strong, especially during stable economic conditions.

Overleveraging happens when a company takes on more debt than its cash flow, assets, or overall risk capacity can reasonably support. In some circumstances, where leverage is used correctly, funds are borrowed and invested in projects that generate steady income. At the same time, the company maintains safe repayment levels and strong financial ratios. In overleveraging, a business uses too much debt in its operations, more than it can generate, so it is unable to repay or even service its debts. Overleveraging stretches a company’s ability to repay, weakens its financial position, and reduces its flexibility to respond to challenges.

Understanding Financial Leverage

Financial Leverage refers to the use of borrowed funds to finance business activities and investments to increase returns to shareholders, rather than depending only on owners’ funds. A leveraged company includes debt as part of its capital structure. It aims to earn more from its investments than it pays in interest, according to the Editorial team. When a business’s returns exceed the interest paid on debt, the return on equity (ROE) increases. For instance, if a business borrows money at a 10% interest rate and invests it in a project that earns an 18% return, the difference between the two rates increases shareholders’ profits.

What Is Overleveraging?

A study by Will (2021) highlights that “overleveraging happens when a business takes on more debt than it can realistically manage based on its equity, their earnings and the operating cash flow. The problem is not simply having debt, but having debt that is too large compared to the company’s ability to repay it under both normal business conditions and difficult economic periods.”

It is important to distinguish between high leverage and excessive leverage. High leverage can sometimes be planned and controlled, especially in industries that require large investments and generate stable, predictable cash flows. In such cases, companies may safely use structured borrowing. Excessive leverage, however, occurs when debt goes beyond reasonable risk limits. This often happens when repayment depends heavily on optimistic sales forecasts, favourable market trends, or the assumption that loans can always be refinanced. Under these conditions, even small economic shocks can create major financial instability.

The Benefits of Financial Leverage in a Business

In corporate finance, debt is not automatically harmful; it can increase company value, improve capital allocation, and support faster growth. The benefits of financial leverage occur when borrowing costs remain affordable, and the returns generated by investments exceed the cost of that debt. A study by Javier (2025) highlights the benefits of leverage on businesses.

a) Increase in the Shareholder Returns

Leverage increases return on equity (ROE) when the return on invested capital (ROIC) is greater than the cost of debt. By using borrowed funds to invest in profitable projects, a company can earn more income compared to the amount invested by shareholders. This multiplying effect on returns is one of the main reasons companies include debt in their capital structure.

b) Raising Capital Without Dilution of Ownership

Debt financing allows a business to raise funds without issuing new shares. Unlike equity financing, which reduces existing ownership percentages and voting power, borrowing keeps ownership and control in the hands of current shareholders. For founders and investors, leverage enables the business to grow while maintaining decision-making authority.

c) Tax Shield Advantages

In many countries, interest payments on debt can be deducted from taxable income. This creates an interest tax shield that lowers taxable income and reduces the overall cost of financing. Because of this tax benefit, moderate, well-planned debt use can increase company value when managed properly.

d) Acceleration of Business Growth

Leverage enables companies to take advantage of growth opportunities such as entering new markets, introducing new products, or increasing production capacity without waiting to accumulate profits over time. In competitive industries, quick access to funding can determine whether a company gains or loses market share.

e) Strategic Acquisition of Assets

Leverage allows businesses to acquire important assets, such as technology, intellectual property, infrastructure, or even competitors. These strategic investments can strengthen long-term competitive advantage. When acquisitions are carefully evaluated and properly managed, debt-financed expansion can improve economies of scale and increase operational efficiency.

Why Businesses Overleverage

Overleveraging occurs out of deliberate decisions influenced by market conditions, management mindset, competition, and weak financial planning. Companies often decide to take on more debt as necessary for growth or even survival. Still, they must consider the effects it may have on the entity. The following are the reasons why businesses take on excessive debt.

- Rapid Expansion Strategies

The eagerness to achieve rapid growth may tempt a business to borrow more than it can manage. An entity that aims to expand quickly by entering new markets, acquiring other firms, diversifying products, or expanding infrastructure will often rely heavily on borrowed funds. If growth outpaces reliable cash flow, debt repayments become harder to manage. Additionally, when the above investments do not produce positive cash flows, over time, the debt that once seemed manageable can quickly become overwhelming.

- Overconfidence in Future Revenue

Confident revenue forecasting often leads to overleveraging. Revenue forecasting occurs when management makes borrowing decisions based on expected market gains, assumptions of economic stability, and high-growth revenue projects. This optimism can lead to debt plans built around best-case scenarios rather than realistic, tested assumptions. When actual performance falls short, the business struggles to meet its repayment obligations, hence overleveraging.

- Poor Risk Assessment

Effective financial management requires planning for potential setbacks, such as economic slowdowns, demand drops, supply chain disruptions, or increases in interest rates. Companies that fail to account for these risks often underestimate potential problems. Without sufficient cash reserves and backup plans, even moderate disruptions can turn previously manageable debt into a serious financial burden.

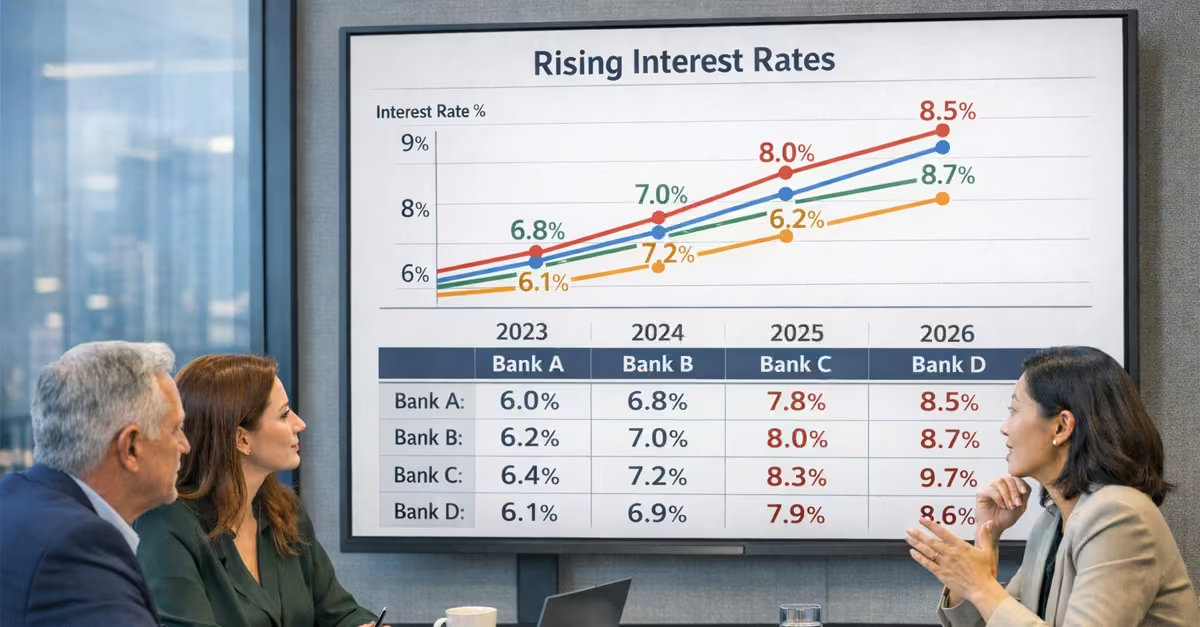

- Sudden Change in Interest Rate

During periods of low interest rates, borrowing is cheap, making borrowing attractive and encouraging firms to take on more debt. During a low-interest period, repayment costs are low, so businesses can easily manage their loans, leading to managed leverage. However, as interest rates eventually rise, refinancing debt becomes more costly, putting increasing pressure on companies with floating-rate loans. Many businesses overextend themselves during low-rate periods and face difficulties when conditions tighten.

- Competitive Pressure

In highly competitive markets, companies may borrow aggressively to maintain their position. The fear of falling behind your rivals, especially in fast-moving or technology-driven industries, can push firms to invest heavily in innovation, marketing, and acquisitions. While some borrowings are strategic, when decisions are driven by competitive anxiety rather than financial discipline, it increases the risk of overleveraging.

Read Also: Risk Management in Business Investments: How to Protect Your Capital

Warning Signs of Overleveraging

Financial stress usually develops gradually, and businesses usually show measurable signs of strain in liquidity, solvency, and market confidence before reaching a crisis point. Identifying these warning signs early allows management and stakeholders to take corrective action and reduce the risk of insolvency.

a) Rising Debt-to-Equity Ratio

A steadily increasing debt-to-equity (D/E) ratio indicates that a business is relying more on borrowed funds to finance growth than on retained earnings or equity contributions. While each industry has its own acceptable D/E benchmarks, sudden or sustained increases beyond sector norms suggest that financial risk is rising. For instance, even capital-intensive businesses that typically carry higher debt levels may become weak if debt grows faster than their earnings, thus leaving the firm exposed to repayment difficulties during downturns.

b) Declining Interest Coverage Ratio

The interest coverage ratio measures how easily a company can pay interest from its operating profits. A declining ratio, particularly below levels of 2.0 in many industries, indicates that interest payments are becoming harder to meet. This decline often signals shrinking financial flexibility and rising difficulties in loan repayments. Factors such as earnings volatility, higher interest rates, or additional debt can worsen this situation quickly. A falling coverage ratio is therefore an early warning that debt may be reaching unsustainable levels.

c) Persistent strain in Cash Flows

Even if a company reports profits, it may still face liquidity challenges. Persistent cash flow strain occurs when operating cash flow consistently falls short of projections or when free cash flow becomes negative while debt obligations remain fixed. This makes it difficult for the company to cover routine expenses, such as payroll, supplier payments, and scheduled loan repayments. Unlike accounting profits, which can be influenced by non-cash items, cash flow metrics reflect the actual ability to meet obligations and are therefore critical for identifying financial stress early.

d) Reliance on Short-Term

When a company repeatedly relies on short-term borrowing or new loans to pay off existing debt, it signals overleveraging. This “rolling debt” approach can be sustainable in stable markets but becomes dangerous when credit conditions tighten and interest rates rise. The dependence on continual refinancing reduces financial flexibility and leaves the company exposed if lenders limit access to new capital. This is particularly concerning for firms with high debt levels relative to earnings, as any disruption in funding can quickly result in a solvency crisis.

e) Reduction in the Credit Rating

When credit ratings from institutions like Moody’s and Fitch are reduced, it is an indicator of increased default risk. Lower ratings lead to higher borrowing costs, restricted access to capital markets, and potential breaches of loan covenants. Even a revision in outlook, from stable to negative, is a warning that lenders perceive growing risk.

f) Market and Operational Distress

Financial markets often detect risk before internal reports reflect it. Indicators such as declining stock prices, widening bond yield spreads, falling investor confidence, and reduced analyst support suggest the market perceives greater leverage risk. On the other hand, operational signs also provide early warnings. Indicators like late payments to suppliers, stricter trade credit terms, and strained vendor relationships reflect pressure on cash flows and liquidity.

The Major Financial Risks of Overleveraging

Debt is a useful tool for enhancing business growth when managed wisely. Still, over-leveraging turns it from a growth tool into a structural liability. In favourable conditions, moderate leverage boosts returns. On the other hand, excessive borrowing creates fixed financial commitments that persist regardless of revenue performance, thereby increasing financial risk. A study by Jody (2025) highlights the following financial risks.

- Cash Flow Strain

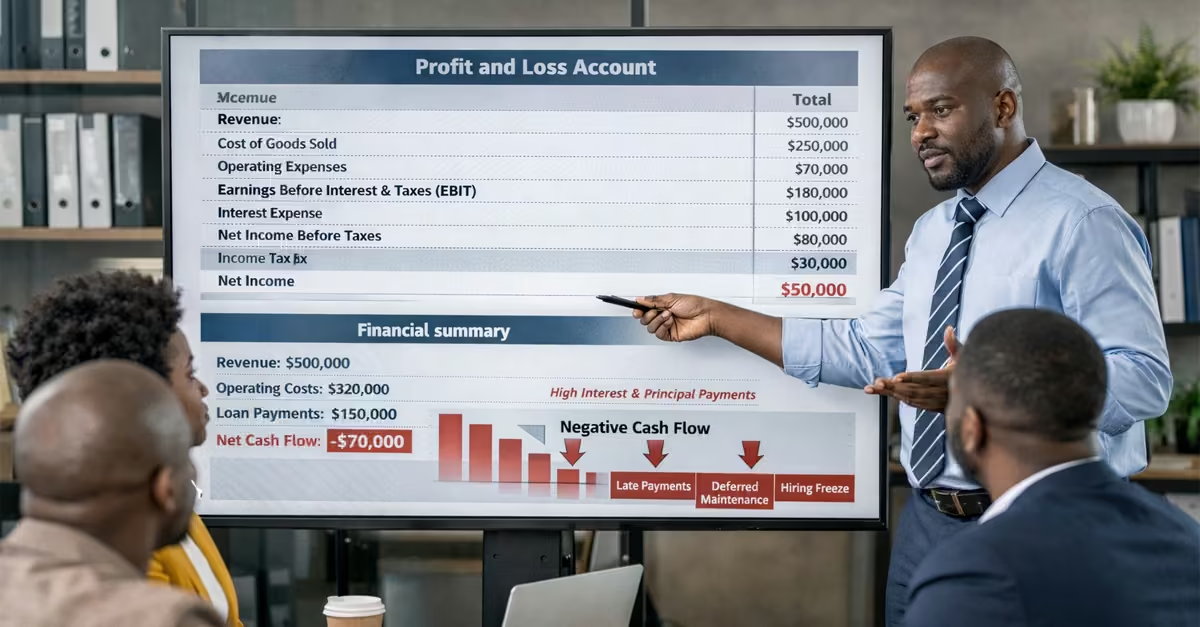

When a business borrows funds, it is obligated to pay fixed interest and principal, regardless of its performance. In contrast, operating costs can often be adjusted in lean periods. Debt payments are inflexible. When debt levels increase, the business diverts more of its earnings to pay interest and principal than to support core business activities.

This strain on cash flow limits operational flexibility, leading to delays in paying suppliers, delaying maintenance, and reducing workforce investment.

- Declining Profitability

Interest payments reduce net income directly. As debt use increases, interest consumes a greater share of earnings, thereby compressing profit margins and lowering key performance metrics such as net margin and return on assets (ROA). Even stable revenue streams can fail to generate healthy profits when debt obligations are high, as much of the earnings is used to pay interest and principal.

When interest on borrowing is taken into account, it will further affect the business’s earnings, especially for a business using variable-rate debt. Higher financing costs, driven by higher interest rates, can quickly reduce earnings per share (EPS) and retained earnings.

- Increased Vulnerability to Economic Shocks

Businesses that heavily depend on debt in their operations are highly prone to economic volatility. During recessions, declining revenue combined with fixed debt obligations puts extreme pressure on cash flow. Market disruptions, such as falling demand, regulatory changes, or fluctuating commodity prices, can quickly impair the ability to meet obligations.

- Insolvency and Bankruptcy Risk

When liabilities exceed a company’s ability to meet obligations as they come due, it leads to insolvency. This is due to persistent liquidity shortages, breached covenants, and failed refinancing attempts, all of which lead to bankruptcy.

- Reduced Access to Future Financing

Excessive use of debt in a business reduces its creditworthiness. Indicators such as worsening financial ratios, declining interest coverage, and higher default risk can trigger credit rating downgrades, leading to higher borrowing rates and limiting access to funds.

As debt levels increase, investor confidence decreases. At this point, the equity investors may demand higher returns to offset risk and lower the price of business stocks. Additionally, lenders may impose stricter credit terms, shorter loan maturities, or higher interest rates, making it difficult for a business to access credit funds.

Read Also: Budgeting Tips Every Business Must Apply

How to Use Debt Strategically

This is the use of borrowed funds to enhance growth, rather than as a short-term solution to cash shortages. When debt is planned carefully, it can help a business expand operations, invest in profitable opportunities, and strengthen its competitive position. However, this requires a clear understanding of available debt options, alignment between borrowing and defined business goals, and disciplined financial management to prevent overextension. The following are ways to use debt strategically in line with the Assured strategy.

- Understanding Debt Types-the starting point for strategic borrowing is understanding the different types of debt instruments available. Debt can be secured or unsecured. Secured loans typically offer lower interest rates because they are considered less risky. Unsecured debt, on the other hand, also carries higher interest rates due to increased lender risk. Knowing these differences enables decision-makers to choose financing structures that align with their risk tolerance, repayment capacity, and operational needs.

- Assessing Growth Needs– Strategic borrowing begins with a realistic evaluation of the company’s growth objectives. Management should clearly define the business’s aims. These objectives must be supported by measurable data, such as historical sales performance, market demand analysis, and internal production capacity, to ensure funds are invested in the right opportunities.

- Forming a Debt Strategy– After defining growth priorities, the business must design a borrowing plan that directly supports those goals. This involves determining the exact amount of funding required, selecting the most appropriate type of debt, and negotiating repayment terms that remain manageable under realistic financial projections.

- Managing debt responsibly– Borrowing is only one part of the strategy; having disciplined management is important for using debt strategically. Companies should regularly monitor financial indicators such as debt-to-equity ratios, interest coverage ratios, and cash flow coverage to ensure leverage remains sustainable.

Conclusion

Debt is a powerful financial instrument that can accelerate growth, optimize capital structure, and enhance shareholder returns when used with discipline and strategic intent. However, excessive debt use can result in various financial risks to the business, such as reduced profitability, strained cash flow, exposure to economic shocks, insolvency, and reduced access to finance. You can easily tell when your business is using excessive debt by observing indicators such as increased debt-to-equity ratios, weakening interest coverage ratios, reliance on refinancing, and lower credit ratings. Debt can be used strategically to enhance growth and increase shareholders’ earnings by applying principles such as understanding the types of loans a business is taking on, developing a debt strategy, and analysing a business’s growth needs before taking on a loan.